By Business Insider Reporter

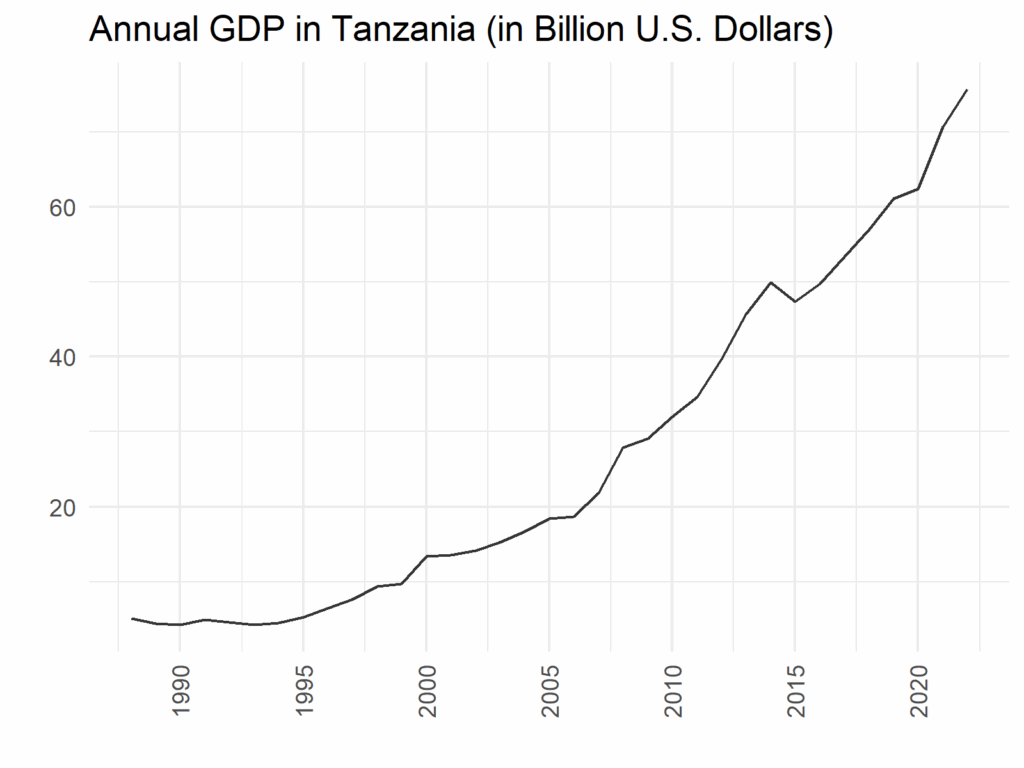

Behind the daily headlines on growth, inflation and trade balances, a quieter but increasingly revealing set of indicators is offering insight into how Tanzania’s economy is evolving.

Payments and collections data, once viewed largely as a back-office banking function, is now emerging as a real time mirror of economic activity. It shows who is transacting, at what scale, through which channels and with what degree of confidence in the financial system

Between 2024 and 2025, recorded payments grew modestly in volume from about 490,000 to 523,000 transactions, an increase of 6.7 percent. Over the same period, however, the total value of those transactions surged from TSh 4.8 trillion to TSh 7.2 trillion, representing growth of nearly 50 percent.

Economists say the divergence between transaction volume and value is significant.

“This pattern suggests the economy is not simply getting busier but maturing,” said Nelson Swai, Head of Information Technology at Stanbic Bank Tanzania. “We are seeing a shift towards higher value, more institutional transactions alongside deeper adoption of digital payment channels.”

Traditionally, growth in transaction volumes has been driven by retail activity, frequent low value payments linked to daily consumption. While this remains important, the faster growth in transaction value points to rising corporate, government and cross border activity.

“When transaction values rise faster than volumes, it usually means businesses and institutions are settling larger obligations digitally,” Mr. Swai said. “That reflects growing trust in the resilience, security and reliability of payment systems.”

This shift mirrors broader economic developments. Tanzania’s heavy investments in infrastructure, logistics and energy naturally generate large payment flows.

As projects move from construction into operational phases, digital platforms are increasingly used for contractor settlements, supplier payments and revenue collection.

Analysts say if this trajectory continues, transactional systems will play an even more central role as major infrastructure projects move from construction into operational phases.

Railways, ports and energy assets generate sustained and complex payment flows once operational, requiring systems that can handle scale, reliability and integration across public and private actors. In that context, the strength of transactional banking will increasingly shape how efficiently infrastructure investments translate into economic activity.

Government collections go digital

One of the clearest signals in the data comes from government collections. Between 2024 and 2025, digitally recorded government payments rose from TSh 278 billion to TSh 333 billion, growth of about 20 percent.

The Ministry of Finance has consistently pushed for digitalisation of public revenue collection to improve efficiency, transparency and compliance. Analysts say the numbers suggest that policy direction is beginning to translate into practice.

“Digital government collections reduce leakage and improve cash management,” said a public finance analyst based in Arusha. “Sustained growth in these channels reflects both institutional reform and taxpayer adaptation.”

According to Stanbic, closer integration between banks and government systems has reduced reliance on manual processes, making it easier for businesses and individuals to meet their obligations digitally rather than through paper based methods.

Beyond aggregate figures, sector level data paints a more nuanced picture of economic activity. Three areas stand out: telecom and media, consumer trade and China related transactions.

Telecom and media payments recorded the largest absolute increase, rising from TSh 1.2 trillion in 2024 to TSh 2.1 trillion in 2025, growth of about 75 percent.

Analysts link this to the continued expansion of mobile money ecosystems, digital content consumption and subscription based services. Telecom platforms are no longer just communication tools but increasingly operate as financial ecosystems embedded in daily life.

The consumer sector also showed strong momentum, with transaction values rising by just over 30 percent to TSh 1.3 trillion. This reflects the steady rise of digital commerce, formal retail payments and supply chain settlements in fast moving consumer goods.

China related trade recorded some of the fastest growth, with transaction values rising from TSh 697 billion to TSh 1.1 trillion, pointing to expanding trade flows and more structured cross border settlement mechanisms.

For businesses, the shift toward higher value digital settlements is already changing how liquidity is managed. Faster and more predictable payments reduce working capital strain, improve supplier relationships and allow firms to plan production and inventory with greater certainty.

As more transactions move through formal digital channels, visibility across value chains improves, strengthening discipline and trust between buyers, suppliers and financiers.

Payments innovation meets financing

For banks, these trends are reshaping how transactional services are structured. Rather than serving only as payment processing tools, transactional platforms are increasingly used to understand cash flows, manage risk and support tailored financing solutions.

Tshepo Molete, Head of Transaction Banking for Tanzania at Stanbic Bank’s Corporate and Investment Banking division, said clients are increasingly approaching transactional banking as a platform to solve broader business and sustainability needs.

“Understanding how money moves through a business allows us to structure solutions that reflect real operating realities,” he said. “That can improve pricing, liquidity management and risk assessment.”

Economists say the widening gap between transaction value and volume reflects three broader trends. Confidence in digital systems is growing as businesses move larger sums electronically. Sector consolidation is replacing fragmented cash-based payments with fewer but higher value transactions. At the same time, transactional data is increasingly shaping how financing solutions are designed.

However, analysts caution that higher value digital transactions also increase systemic exposure if systems fail. Continued investment in cybersecurity, redundancy and regulatory oversight remains essential to maintaining confidence. As Tanzania’s economy becomes more complex and interconnected, payments data is no longer just a record of past activity. It is emerging as a forward looking indicator of how trade, investment and growth are evolving.